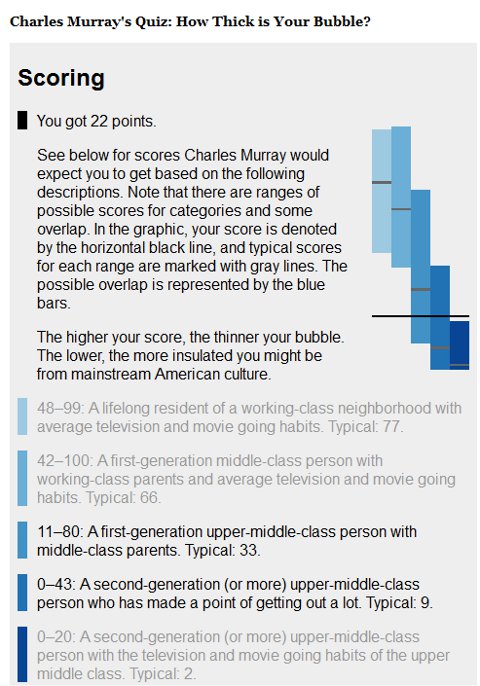

Just for kicks, I decided to take the Murray “Do you live in a bubble” test. Basically the test tries to determine which class you are aligned up with the most closely, and whether you’re a 1st or 2nd gen in that particular class. Try this link: ( “Do you live in a bubble”) to try the online test out!

Okay below are my results and I have to say that the categories that the site test projected is pretty close to where I would put myself within the spectrum.

I think particularly interesting in my case is the fact that my family has shifted out of middle class too, but when I was growing up, we were definitely just middle class. In fact, I refer to myself as “Lower Upper Middle Class” whereas my family (parents and sister’s family) are both solidly Upper Middle Class.

While this test worked for me, I don’t put a lot of merit in such tests, and while the test is designed by a true professor that did some leg work to put together a decent test, one size does not fit all. Upper Middle Class has different meanings depending upon where you live, and your culture.

Try the link above, it may be amusing for you too…

Yeah, I know, it a funny title “Lower Upper Middle Class“, but it’s the closest representation to a socioeconomic class that I could come up with to represent my current state.

So what does it mean to be “Lower Upper Middle Class”?

I like to think of it as being at a party where there are two connected but different rooms. Room 1 is where my middle-class friends are talking, and I’m mostly in this room. Room 2 is where some of my Upper Middle-Class friends and even family members are talking about topics I want to hear. While I want to join the conversations with my friends in Room 2, my friends in room 1 and room 2 don’t get along. So I’m standing in the doorway of rooms 1 and 2 acknowledging some of my friends in room 2 and desperately trying to listen to what they are saying while hanging out talking to my friends in Room 1 at the same time.

I guess in some ways, I don’t belong to either room. You see, I’m still in a metamorphose phase where I’m trying to grow my money to a level that I can participate in more Upper Middle-Class Activities without decreasing my net worth, while at the same time trying to resist spending money and time on some of the things that my middle-class friends are spending money on. I’m pretty much in the proverbial “Catch-22” stage in my financial life right now.

Okay, now that I explained the feeling of “Lower Upper Middle Class“, what are the other points of interest that I perceive about my current stage?

Vacations: I can afford to go on better and more vacations, including vacations overseas, but I don’t. I want to establish a more secure financial footing before I take that leap. For me, I mustn’t spend money, which in effect will decrease my wealth. This is where a dividend strategy comes into play. Read how I’m doing such a strategy for my lunches at work via my article about the Dividend Lunch Experiment. So for the time being, all my vacations are local to the US.

Community Activities: We do community activities now, especially my wife where she volunteers and does charity work for the Schools and community in general. I hope to expand my role in this area too, but for now, I continually try to think of ways to better my financial picture.

Paying for College for the Kids: This is one of the many drains I have on my paycheck. I want to fully fund my kid’s college costs. This will give them a huge head start in life. Both of my kids are doing great in school, and I’m hoping they get scholarships of some sort.

House Hunting: Currently I’m mortgage-free, but I want to upgrade to a larger house. Since I’m deal-oriented and picky, I’ll be looking for a long time. I hope the rates stay low for a long time too. It’s funny, I can afford a more expensive house, but I choose not to. Perhaps if I had just a bit more money I would take the plunge and buy a dream home…

Eating Out: This is one area in which we splurge. We go out 2 or 3 times a week to a decent restaurant, but usually, it’s a chain restaurant like Olive Garden, Red Lobster, Chinese or Mexican restaurants too. But by a large margin, we go to Panera restaurant the most. Healthy food, but affordable for the most part. (Healthy, in that I usually get the Chicken Cobb Salad with Avocado, yum!).

Cashflow constrained: Although my house is paid off, I redirect the freed-up money to my 401k, Roth IRA, and ESPP options. All three are great, but my take-home pay doesn’t go very far. I’m especially proud that I participate in the ESPP plan at work because it’s a great money hack that makes me a few extra thousand in free money, and is a forced saving mechanism. How cool is that! Read this clever way that I’m using my ESPP to fund my Roth IRA.

Fashion: The entire house buys better clothes, except me. I don’t mind though, I need to polish my look by losing extra weight anyway.

Entertainment: We do go to the movies to see interesting-looking movies, but mostly we just wait until the movies come out on DVD. We do other things too, and this will continue to expand as I develop a strategy (more than likely dividends) to fund more adventures in entertainment.

Okay, I’ve just scratched the surface of what it’s like to be “Lower Upper Middle Class”, but it’s already past midnight, so I’m going to say good night!

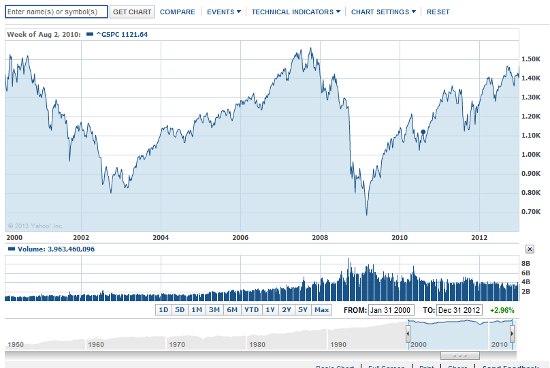

Okay, I’ve noticed a belief going around for the past few years that I feel that I have to write about to dispel the notion that the stock market is broke and not worth participating in!

Both an individual I know, and the media in general has called the past 10 or so years a “lost decade” from an investment standpoint. This is not true, and I’ve been able to achieve over an 8% annual return during the time that the media gurus kept stating that the market has disappointed for the past 10+ years.

Before I start my explanation as to why they are wrong, let me present the S&P 500 chart for the past 10+ years…

Not pretty huh!

Why You Should Still Invest In The Stock Market

You can see why the media is calling it the “lost decade”… If one were invest all their money all at once (this is called a lump sum) in either year 2000 or at the end of 2007, and not invest any other money, then it’s true, it would have been a lost decade.

But more than likely, you had a 401k plan that would dollar cost average out your contributions during the year. And these stock market dips created an opportunity instead of a flat “lost decade” period of time.

To be honest, my conviction in this “opportunity” was so strong that I increased my contribution amount during the dips that started back in 2008. The amount I increased my contributions was only a few extra percentage points though, so I don’t attribute my over 8% gain to it.

My buddy at work even did better. He’s a young guy and started investing in 2007, and when the 2008 stock market dropped like the bottom fell out, he was discouraged and said he was thinking about stopping his contributions and even pulling his existing money in his 401k (this would have been a huge mistake if he did). I explained to him, the advantages of staying in and told him that I was increasing my contribution amount. Then I explained to him how I was jealous because he was just starting and was going to be able to buy shares of stocks at a huge discount. I even called it a once in a lifetime opportunity. He said I wear rose-colored glasses, and perhaps he’s right, but he didn’t stop contributing and didn’t pull out his money (whew!).

The article on “dollar cost averaging” that I linked to above explains how dollar cost average works, but in case you don’t want to click on it, I’m going to do a quick explanation here.

With an investment instrument like a 401k plan, you buy a set dollar amount of shares of stocks (or really mutual funds) on a repeating periodic basis. In my case that repeating period is every 2 weeks. So when the price of shares of an investment drop in value, I’m able to buy more shares of that investment. This is the magic that enabled me to have an over 8% annual return during the past 10+ years.

To the person not in the know, the past 10+ years in the stock market seem like a tragedy and huge disappointment (aka lost years), but really those dips were great opportunities to buy cheap shares of stocks and mutual funds.

So you will hear people use the chart above to make it sound like the past 10+ years was a huge loss, but really it was a pretty good term, at least in my 401k plan and other stock market investments.

Hope this clears up some confusion as to why it’s still wise to invest in the stock market via a 401k plan.

I hate to say this but my college “Age-Based” 529 plan selection has failed to live up to my expectations.

It seemed like such a brilliant idea 13 years ago. It was an Age-based plan that in theory would re-balance the asset investment types for me based on the age of my kids. To me it seemed like a slamdunk! Unfortunately, the stock market decided to do the exact opposite from the strategy that my state’s college 529 plan was following…. What a huge disappointment!

So, instead of it being a great investment vehicle, at most it’s been a glorified savings account. At least I get to deduct the amount I contribute to it from my state income tax!

Future Concerns:

Now as my kids are growing older, the age-based plan starts to re-balance the money in the plan from equities to bonds. Unfortunately, this is also a bad time to do such a re-balance since the US Treasury rates are rising! As the treasury rates rise, the bond funds should suffer. Obviously this just adds insult to injury!

In fact, the only thing that has worked for me is that I’ve been able to dollar cost average my contributions along the bump stock market road. This at least give my account a bit of a return, but still less than have of what my “all equities” 401k plan has been able to accomplish.

So in conclusion, if you are considering a similar college investment route with your kids and their college 529 planning… I recommend thinking long and hard about other options that just the Age-Based option! If I had to do it over, I wish I would have choose a mix like half in the age-based plan, and half in an “all equities” plan.

It’s not too late for me though, I still might change the strategy since my oldest is only 13 years old.